Sector Spotlight

Grocery Deep Dive Part II

Carbon Arc Data Assets: POS Supermarket, POS Instore & Online, POS Convenience, Digital Advertising, TikTok Shop

Inside the Forces Reshaping Beverages in 2025

January 26, 2026

Executive Summary

Beverage demand remains constrained as grocery spending softens, with spend per store across legacy categories such as soda, seltzer, and beer largely flat or declining amid heightened price sensitivity and discretionary pullback. Consumer behavior is becoming more intentional; most visibly reflected in alcohol consumption sitting near historic lows1 as shoppers reassess discretionary choices. Against this backdrop, pockets of growth are emerging within protein ready-to-drink (RTD), hydration, and energy, but outcomes are increasingly uneven and driven by brand-level innovation, marketing, and go-to-market execution rather than category tailwinds. In response, legacy food and beverage players are accelerating acquisitions of emerging, health-forward brands, signaling where long-term confidence lies. Together, these dynamics point to a market where capital allocation, channel strategy, and consumer relevance - not legacy scale - are increasingly determining winners and losers.

Key Takeaways

-

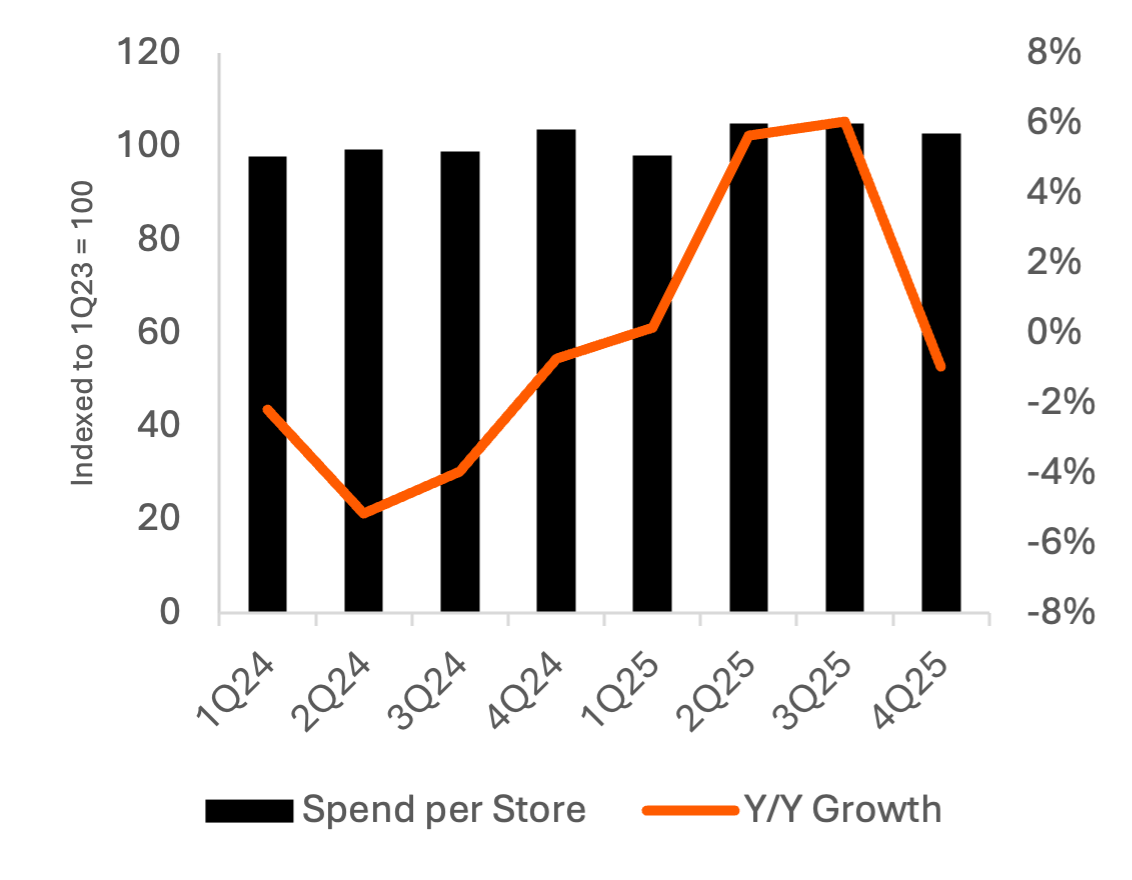

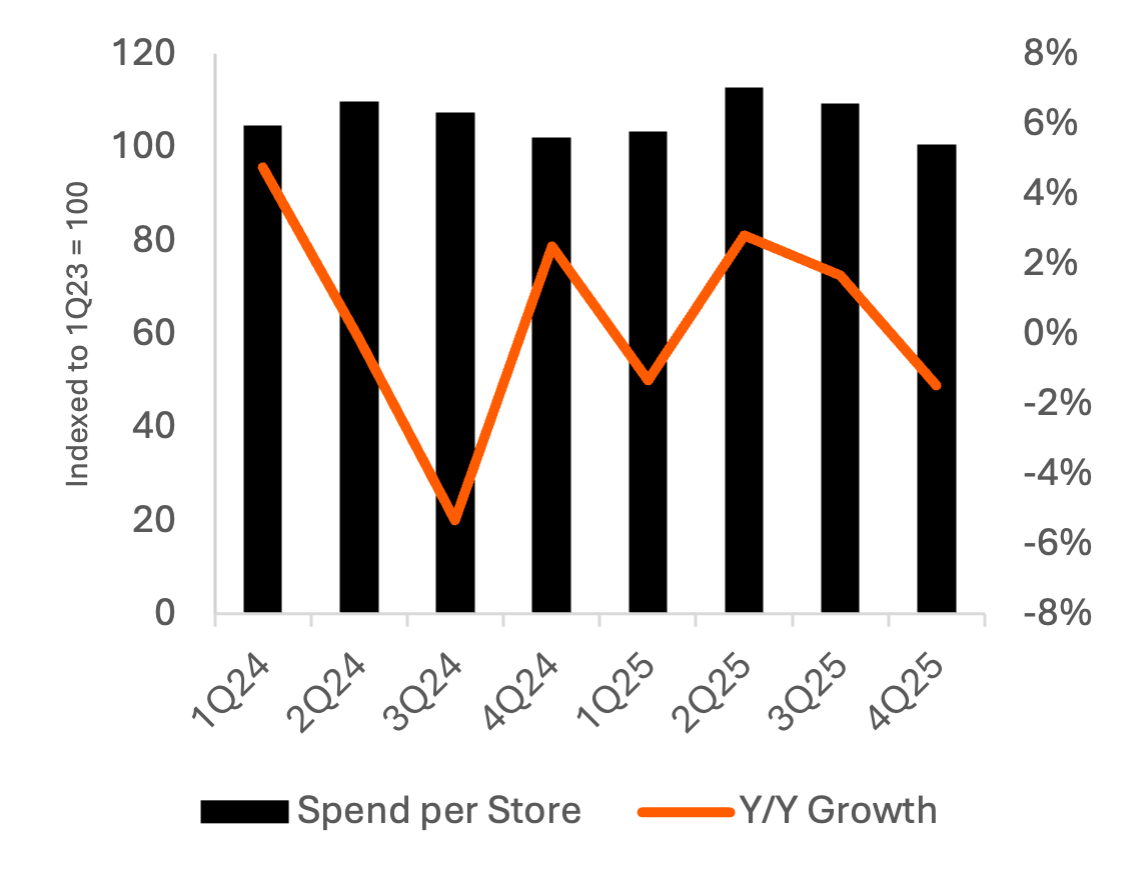

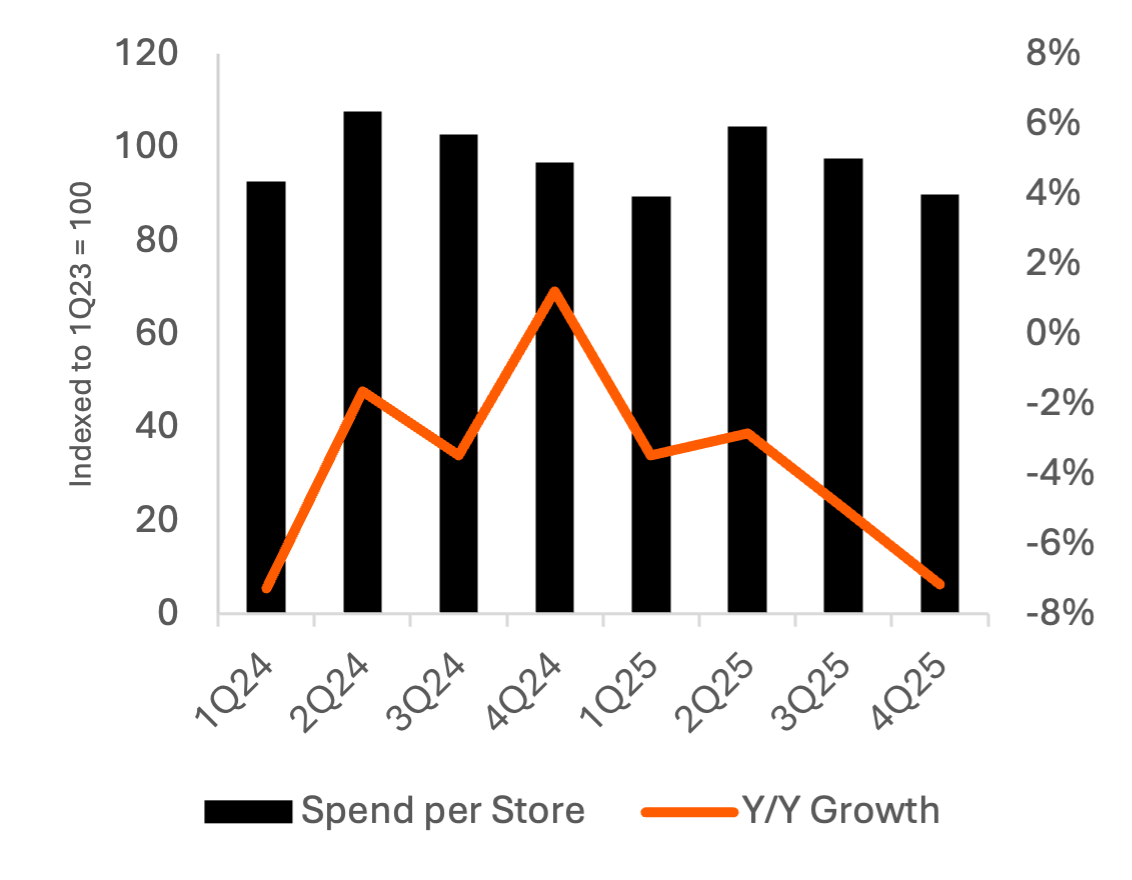

Core beverage categories remain under pressure. Spend per store across soda, seltzer, and beer + hard seltzer is flat to down Y/Y, underscoring continued structural headwinds in legacy categories.

-

Growth is shifting toward functional beverages as consumer preferences evolve. Amid a pressured beverage backdrop, pockets of growth are emerging in protein ready-to-drink (RTD), hydration, and energy, aligning with increasing consumer awareness and prioritization of products offering perceived functional, health, and wellness benefits.

-

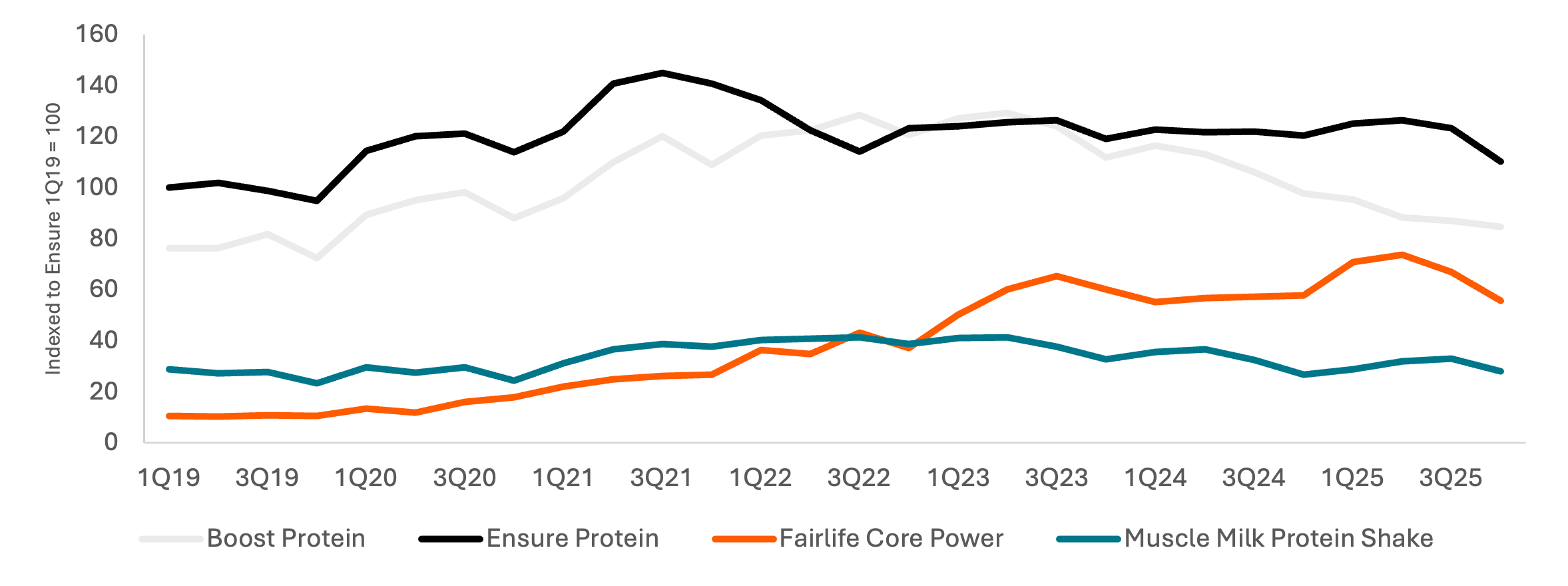

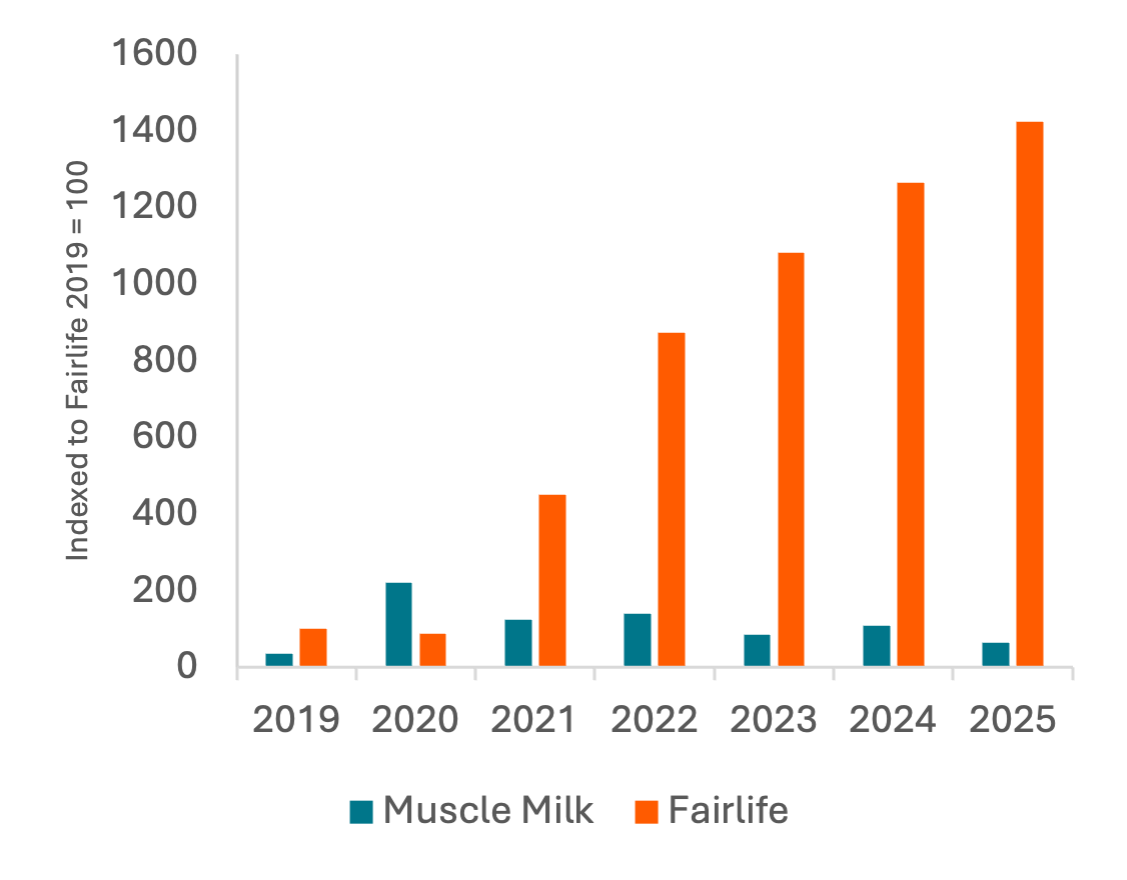

Protein RTD illustrates how brand management choices shape outcomes. Fairlife’s evolution into a billion-dollar brand is underpinned by sustained investment in advertising and distribution, driving multi-year gains in spend per store, while Muscle Milk’s comparatively flat performance reflects a more static investment posture within the same category.

-

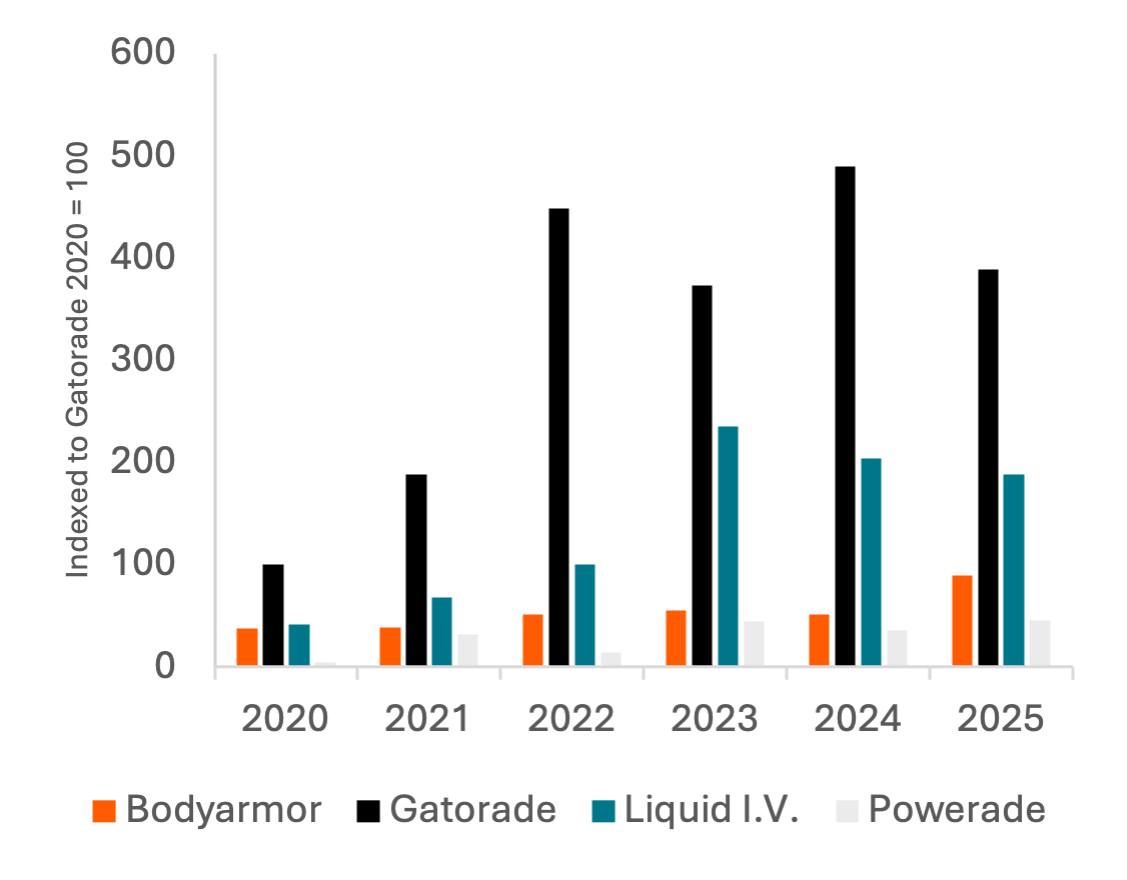

Hydration is emerging as an early case study in social-driven demand formation. Liquid I.V.’s continued growth contrasts with flat performance from Gatorade and Powerade, illustrating how social media–driven virality and cultural zeitgeist can translate into measurable retail inflections and revenue outcomes.

-

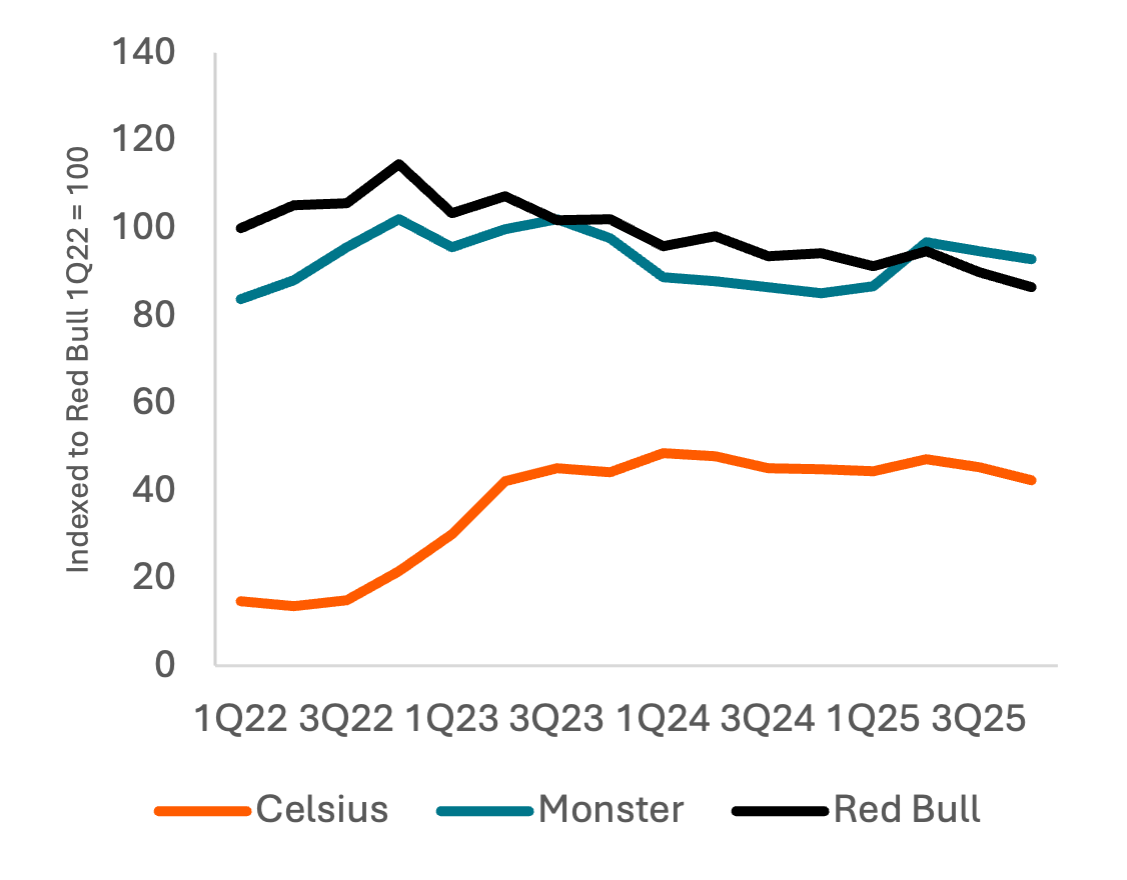

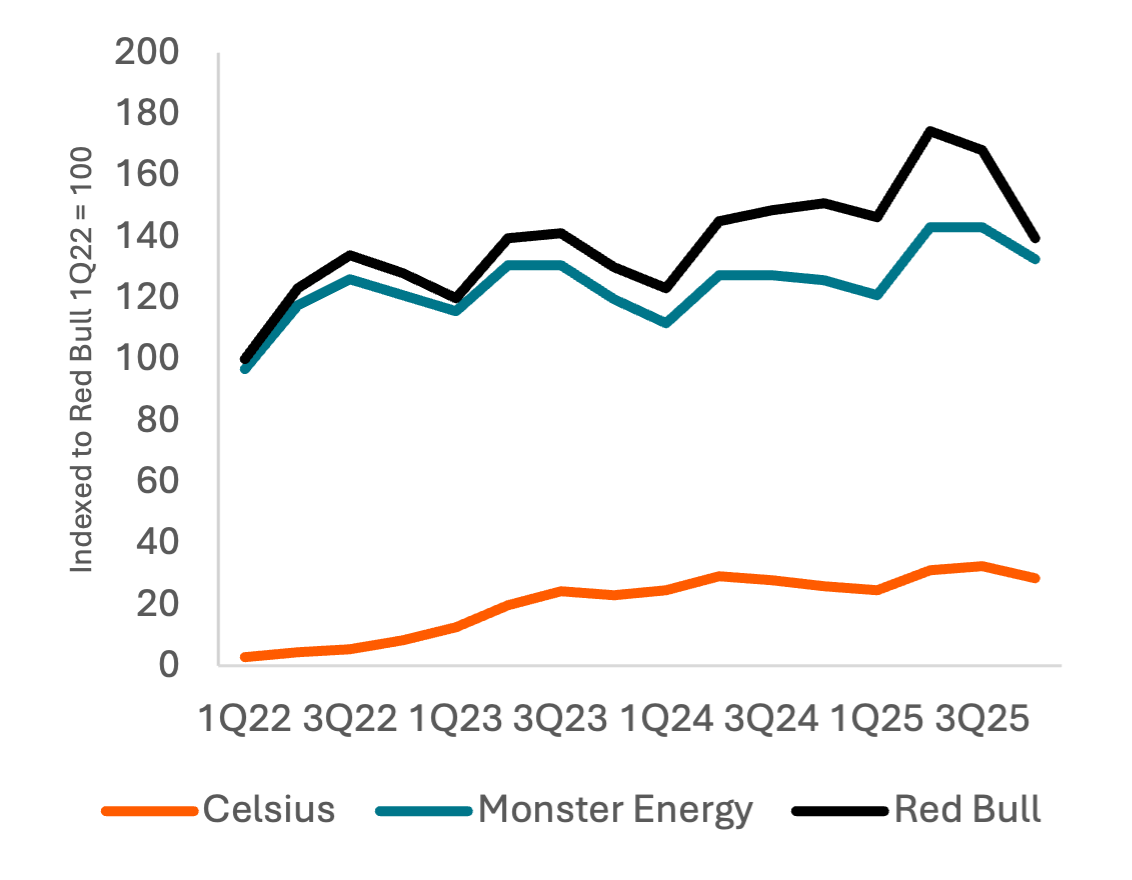

Energy highlights how product innovation can expand categories. Celsius’ sustained growth in spend per store across supermarket and convenience channels underscores how differentiated, health-forward product innovation can drive product-led category expansion by bringing new consumers into the brand, while Monster and Red Bull maintain resilient baseline demand.

2026 Beverage Outlook

The broader beverage market continues to face headwinds as grocery spending softens across retailers against a challenging macro backdrop2. Overall consumption remains near historic lows, with growth across traditional categories - soda, seltzer, and alcohol1 - largely stalled or in decline. As price sensitivity persists and discretionary spending remains under pressure, growth in legacy segments has been difficult to sustain.

At the same time, consumer behavior is evolving. Shoppers are becoming more intentional about what they drink, increasingly prioritizing products that offer perceived functional, health, and wellness benefits3. This shift is creating distinct pockets of growth within an otherwise pressured category, as innovation and brand differentiation matter more than ever.

Legacy food and beverage players are responding with a wave of acquisitions focused on emerging, health-forward brands, signaling where long-term confidence lies.4,5,6,7 Competitive dynamics in the protein RTD, hydration, and energy drink sectors serve as interesting case studies that can inform how legacy F&B should think about positioning their brand portfolios for the future.

Exhibit 1: Soda Average Spend per Store

Source: Carbon Arc POS – Supermarket – CA0047

Price: Requires row-level block data access, available on request

Exhibit 2: Seltzer Average Spend per Store

Source: Carbon Arc POS – Supermarket – CA0047

Price: Requires row-level block data access, available on request

Exhibit 3: Beer + Hard Seltzer Average Spend per Store

Source: Carbon Arc POS – Supermarket – CA0047

Price: Requires row-level block data access, available on request

Protein Ready-To-Drink (RTD)

Protein RTDs offer a compelling case study in how brand management and capital allocation shape category outcomes. Over the last several years, the space has seen rapid product innovation8, expanding well beyond legacy incumbents like Ensure and Boost. Once limited to largely clinical use cases, protein RTDs are now mainstream lifestyle beverages that many consumers have integrated into their everyday routines. Recognizing this shift, major strategics moved quickly.

Coca-Cola acquired Fairlife in January 20209, followed by PepsiCo’s acquisition of Muscle Milk in April 201910. While both brands compete in protein RTDs, Fairlife has scaled into a billion-dollar brand11, leveraging Coca-Cola’s distribution reach and sustained advertising investment. Muscle Milk, by contrast, has seen relatively stable share, suggesting more limited strategic prioritization within PepsiCo’s broader portfolio.

Exhibit 4: Average Spend per Store

Price: Requires row-level block data access, available on request

Exhibit 5: Advertising Spend

Price: Not Available Through Platform or Block Delivery, Requires Custom Build

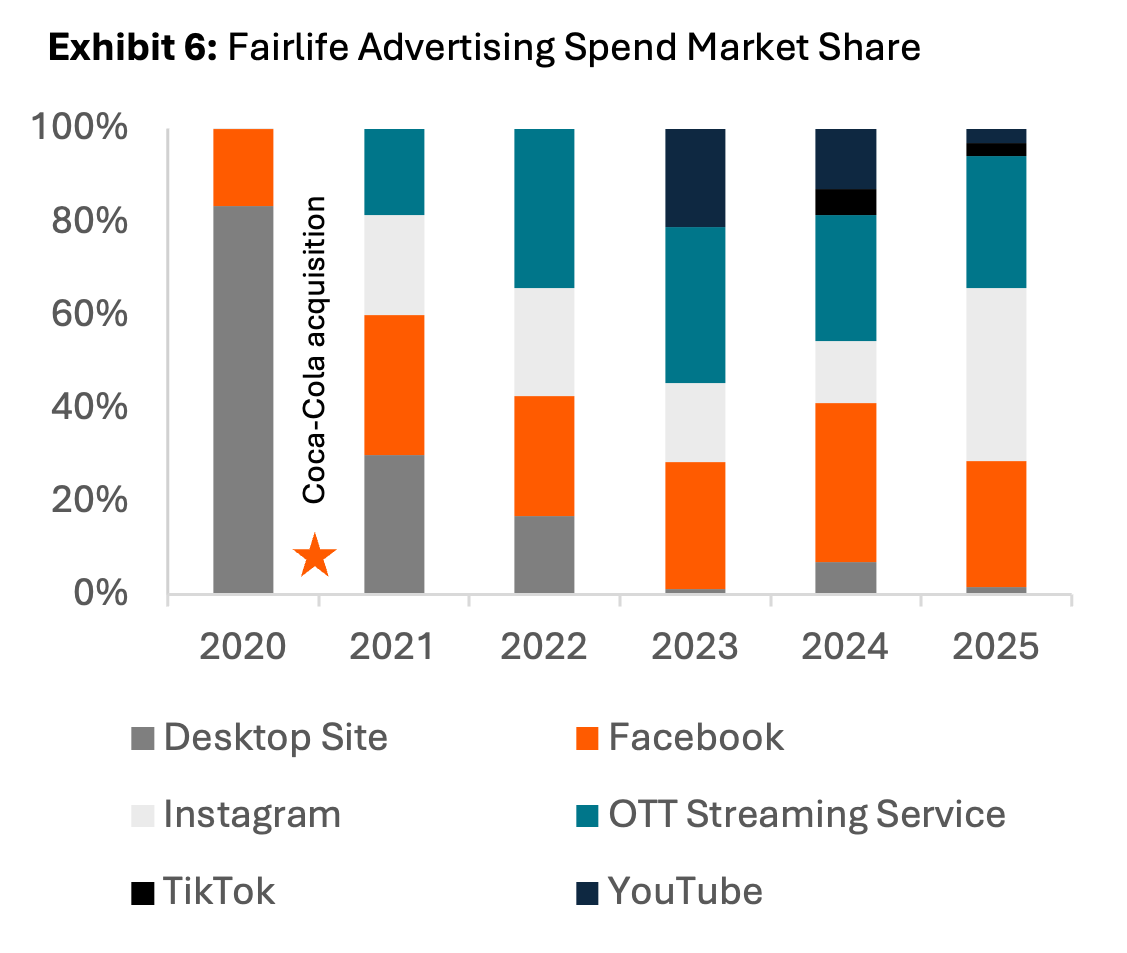

Exhibit 6: Fairlife Advertising Spend Market Share

Price: Not Available Through Platform or Block Delivery, Requires Custom Build

Hydration

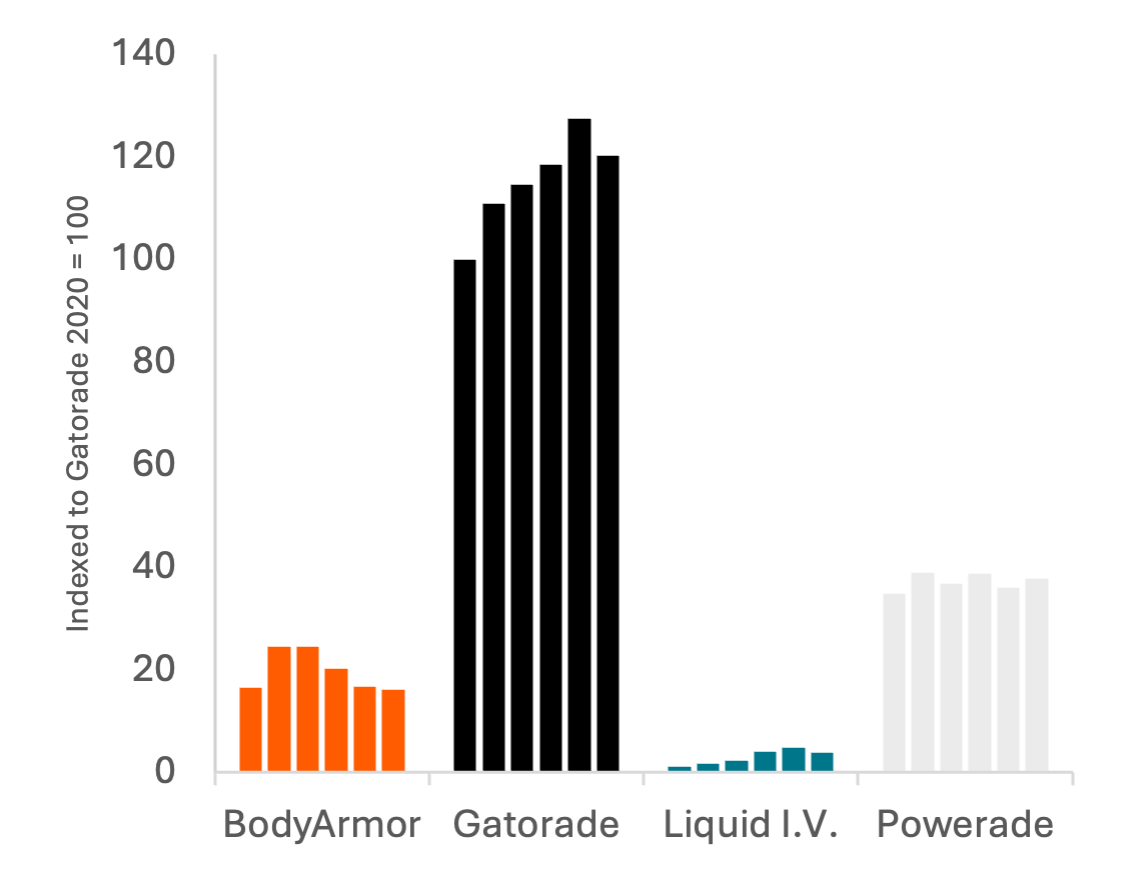

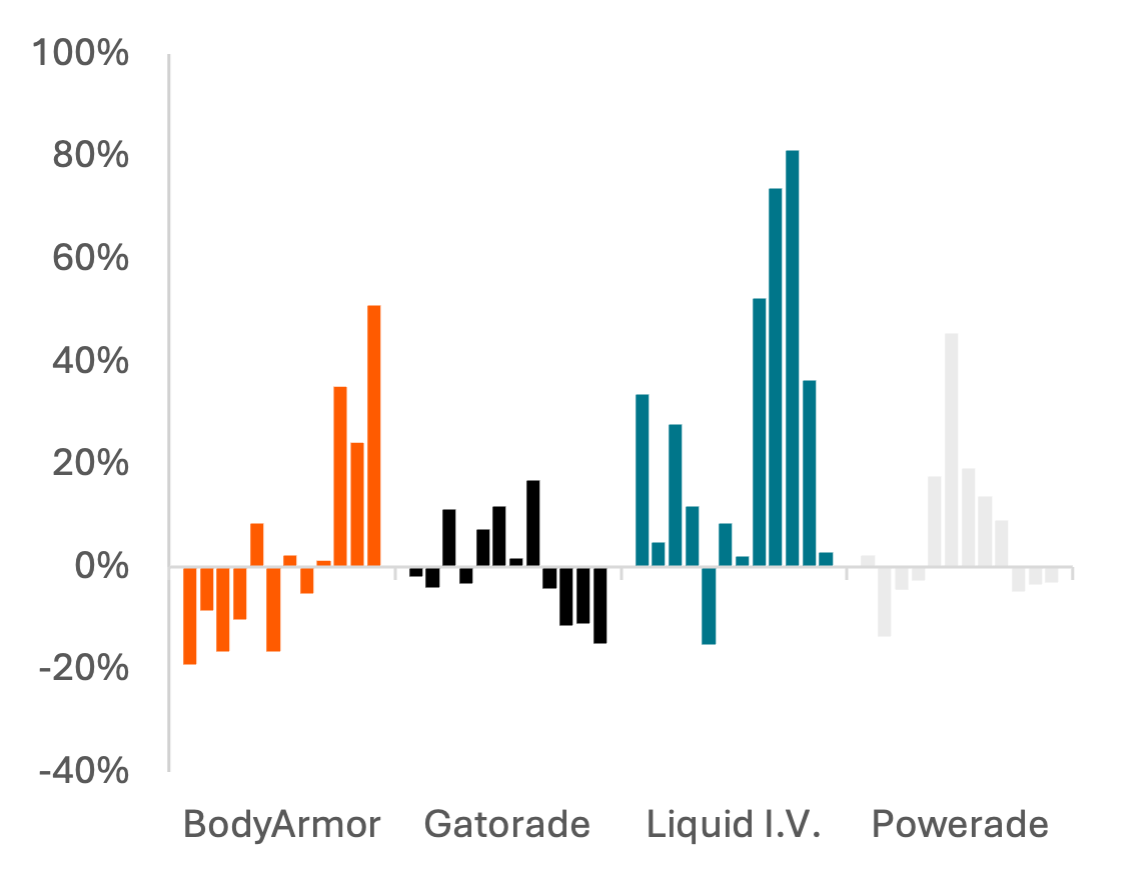

While scale and distribution from large F&B players provide important tailwinds, success increasingly sits at the intersection of product relevance and promotion. Hydration + electrolyte formats continue to gain share, while traditional RTD sports drinks remain stagnant. Hydration + Electrolyes serve as an early case study of how social-media-driven virality and cultural zeitgeist can translate into sustained retail sales momentum.12

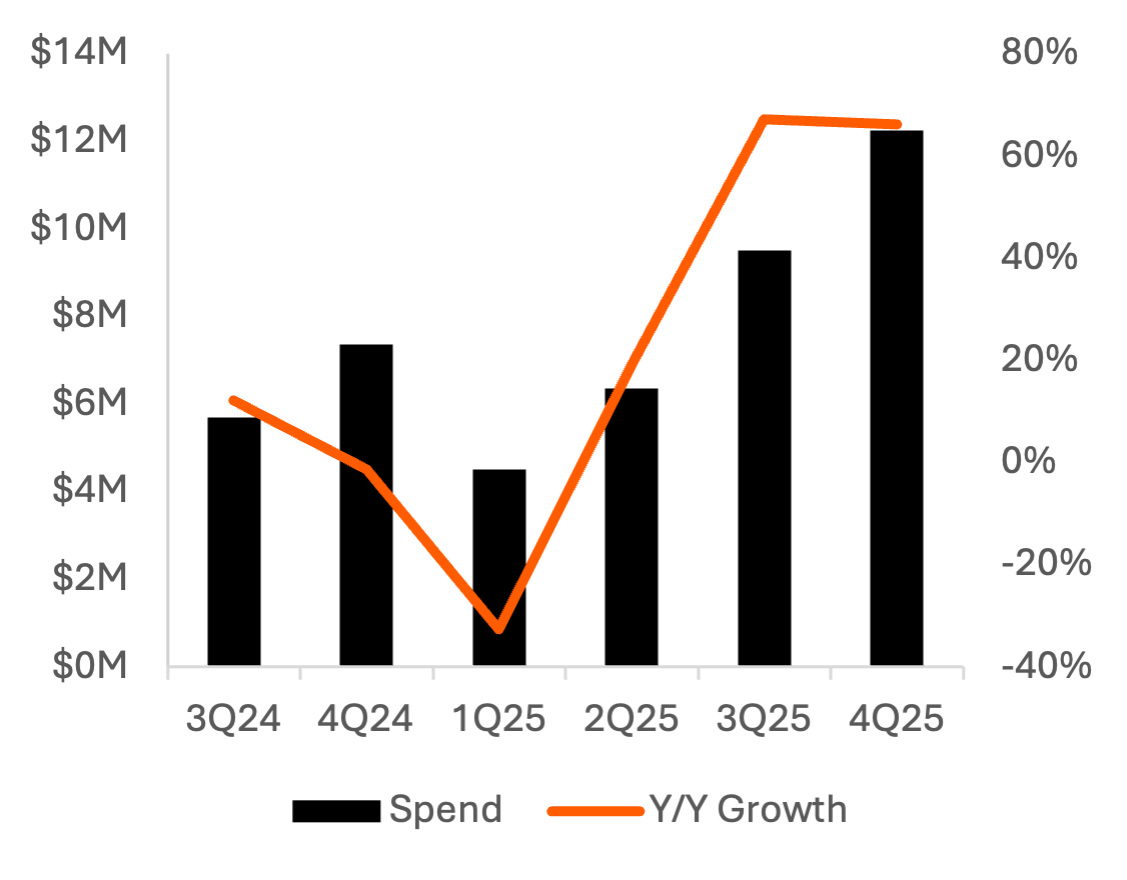

The rapid acceleration of vacuum-sealed flask sales via TikTok Shop reinforces this dynamic, illustrating how social platforms can drive real demand inflections. Sales of BodyArmor, Gatorade, and Powerade remain largely mixed across channels for 2025, while Liquid I.V. continues to grow. This analysis reflects Walmart and a southeastern U.S. grocery chain; we would expect Liquid IV’s performance to be even stronger across other retail channels.

Exhibit 7: Average Spend per Store Yearly (2020 - 2025)

Price: Requires row-level block data access, available on request

Exhibit 8: Walmart Spend Y/Y Growth Quarterly (2023 - 2025)

Price: Requires row-level block data access, available on request

Exhibit 9: Advertising Spend

Price: Not Available Through Platform or Block Delivery, Requires Custom Build

Exhibit 10: United States TikTok Shop Revenue Vacuum Flasks

Price: Requires row-level block data access, available on request

Energy

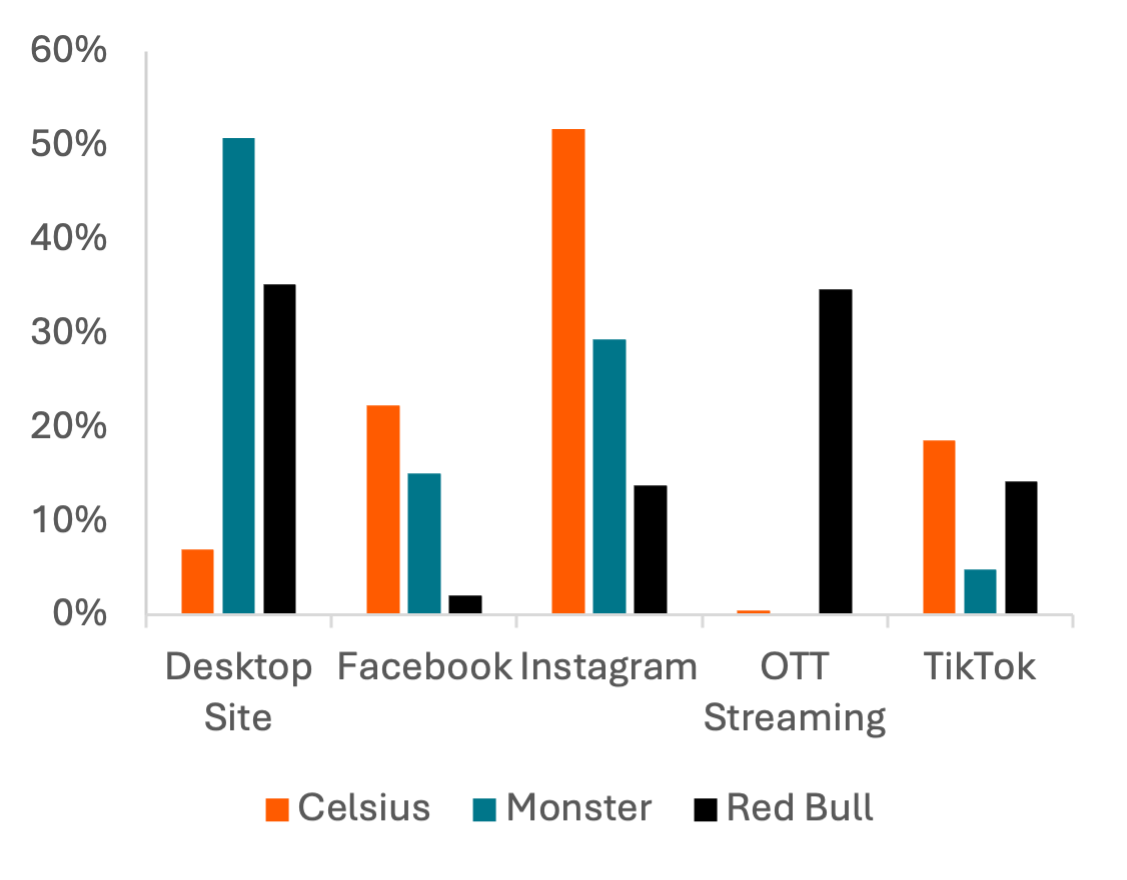

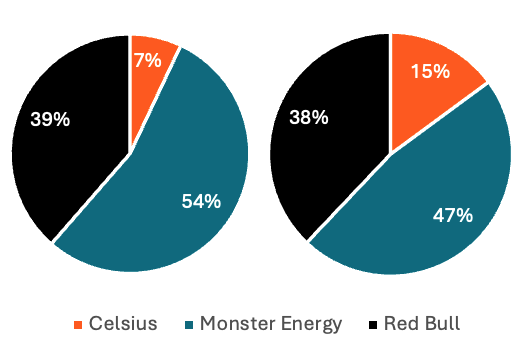

The energy category highlights how innovation can drive incremental demand in mature markets. Celsius has delivered sustained gains in average spend per store across both supermarket and convenience channels, while Red Bull and Monster continue to exhibit structurally stable demand - particularly in convenience, where spend remains elevated. This coexistence suggests category expansion rather than zero-sum brand displacement.

Celsius’ early momentum in 2022 appears to have been supported by a differentiated, digitally native advertising mix relative to incumbents’ more stable media strategies. That go-to-market differentiation coincided with rapid brand scaling and accelerating in-store performance, reinforcing that growth has been driven by innovation and consumer relevance rather than pricing pressure.

Exhibit 11: 2022 Advertising Spend Mix by Platform

Price: Not Available Through Platform or Block Delivery, Requires Custom Build

Exhibit 12: Walmart Spend Market Share 2022 (left) vs 2025 (right)

Price: Requires row-level block data access, available on request

Exhibit 13: Average Spend per Store

Price: Requires row-level block data access, available on request

Exhibit 14: POS Convenience Card Spend

Price: 85.46 Tokens

References

-

Gallup. “U.S. Drinking Rate at New Low as Alcohol Concerns Surge” August 12, 2025. https://news.gallup.com/poll/693362/drinking-rate-new-low-alcohol-concerns-surge.aspx

-

FoodDive. “‘It’s not going to be easy’: Food industry faces uphill growth battle in 2026” January 21, 2026. https://www.fooddive.com/news/its-not-going-to-be-easy-food-industry-faces-uphill-battle-to-grow-in-2/807818/

-

Forbes. “The Rise of Functional Beverages among Millennials and Gen-Z” April 12, 2025. https://www.forbes.com/sites/jesscording/2025/04/13/the-rise-of-functional-beverages-among-millennials-and-gen-z/

-

PepsiCo. “PepsiCo completes acquisition of poppi, accelerating strategic portfolio transformation” May 19, 2025. https://www.pepsico.com/newsroom/press-releases/2025/pepsico-completes-acquisition-of-poppi-accelerating-strategic-portfolio-transformation

-

Flowers Foods. “FLOWERS FOODS, INC. TO ACQUIRE SIMPLE MILLS” January 8, 2025. https://flowersfoods.com/news/news-releases/2025/flowers-foods-inc-to-acquire-simple-mills/

-

Hershey. “Hershey Completes Acquisition of LesserEvil, Expanding Consumer Choice” November 19, 2025. https://www.thehersheycompany.com/en_us/home/newsroom/press-release/2025-11-19-Hershey-Completes-Acquisition-of-LesserEvil,-Expanding-Consumer-Choice.html

-

Celsius. “Celsius Holdings Completes Acquisition of Alani Nu” April 1, 2025. https://ir.celsiusholdingsinc.com/news/news-details/2025/Celsius-Holdings-Completes-Acquisition-of-Alani-Nu/

-

Abbott. “Muscles, the New Flex: Abbott Launches Two New Ensure® Max Protein Shakes to Tap into Growing Muscle Health Movement” December 4, 2025. https://abbott.mediaroom.com/2025-12-04-Muscles,-the-New-Flex-Abbott-Launches-Two-New-Ensure-R-Max-Protein-Shakes-to-Tap-into-Growing-Muscle-Health-Movement

-

Fairlife. “The Coca-Cola Company Acquires fairlife” January 3, 2020. https://fairlife.com/news/the-coca-cola-company-acquires-fairlife/

-

PR Newswire. “Hormel Foods Finalizes the Sale of CytoSport to PepsiCo” April 15, 2019. https://www.prnewswire.com/news-releases/hormel-foods-finalizes-the-sale-of-cytosport-to-pepsico-300832306.html

-

Fairlife. “fairlife is The Coca-Cola Company’s Newest Billion Dollar Retail Brand” February 11, 2022. https://fairlife.com/press-release/fairlife-llc-billion-dollar/

-

CNN. “How America’s obsession with staying hydrated became a $1.5 billion business” May 24, 2025. https://www.cnn.com/2025/05/24/food/hydration-electrolytes-drinks-popularity

Questions?

Contact us at support@carbonarc.co if you have any questions!

CARARC-20260126-GROCERY-0001